- The Ipon Challenge

- Posts

- A Simple Year-End Money Review (So You Know Where You Stand Going into 2026)

A Simple Year-End Money Review (So You Know Where You Stand Going into 2026)

Learn how to review your finances using income, spending, and net worth to understand your true financial standing before setting new-year goals.

Marianne Lim

December 22, 2025

The Second Installment of Our Three-Part Year-End Series

Last week, we talked about the money lessons we’re carrying into the new year.

Before we talk about goals for 2026, we need to slow down and answer a much simpler question: What actually happened this year?

The goal here isn’t precision but being familiar with where you stand financially. I want you to reach a point where your money doesn’t feel mysterious or heavy. .

In this issue, we will help you create a simple personal income statement, year-end spending review, and a year-end net worth snapshot. We also created a template for you if you don’t know where to start. You can find it at the end of this issue.

In today’s edition, we’ll go over:

How to make a simple personal income statement, yearly spending review, and net worth snapshot

We will also explain how these 3 tie together to explain your financial standing

TLDR;

The Bottom Line

Review your money in three parts: total income, yearly spending, and net worth. Together, they show what you earned, what your life costs, and what actually accumulated.

The content

Part 1: Create Your Personal Year-End Income Statement

(A fancy name for a very simple list)

Let’s start with something positive: how much you earned this year. Income is everything that came in, not just your main job.

The above is for visual purposes only! These numbers are hypothetical.

Step 1: List every source of income you had this year

Open your bank app, payslips, or messages. Then list:

Salary from your main job

Side hustles or freelance work

Bonuses, 13th month pay, incentives

Online selling

Cash gifts or one-time income

Step 2: Add them all up

This is your total income for the year. You can’t feel in control of money you’ve never fully acknowledged earning.

Part 2: Do a Yearly Spending Review (Even If It’s Incomplete)

Now let’s talk about where the money went. This is how to do it the simple way.

The above is for visual purposes only! These numbers are hypothetical.

Option A: If you have monthly data

Group your expenses into big categories (rent, food, transport, etc.)

Add up the totals for the year

Option B: If you don’t have monthly data (most people)

Estimate your average monthly spending per category

Multiply each one by 12. See above illustration.

Yes, it’s an estimate. That’s okay. You’re trying to understand the shape of your spending.

Common spending categories to list:

Housing (rent + utilities)

Food (groceries + eating out)

Transportation

Personal (clothes, skincare, etc.)

Subscriptions

Health & medical

Travel

One-time big expenses (repairs, appliances)

Once you’re done, add everything up. Now you know roughly how much it costs to live your life.

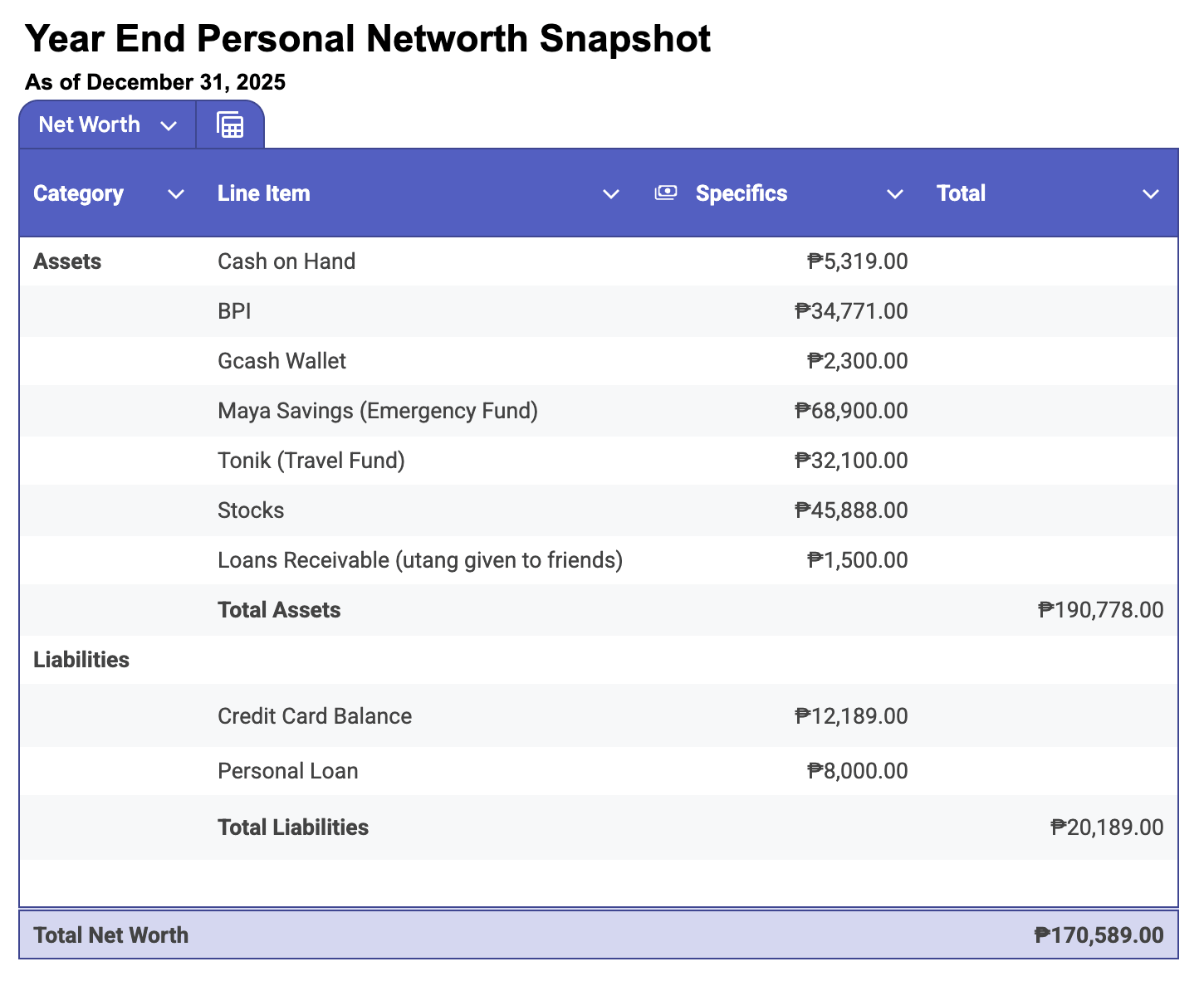

Part 3: Do a Net Worth Review (What You Own vs. What You Owe)

This is where everything comes together.

Net worth sounds intimidating, but it’s just this: What you have – what you owe = your net worth

The above is for visual purposes only! These numbers are hypothetical.

Step 1: List everything you have (Assets)

Write down balances for:

Bank accounts

Checking accounts

Emergency fund

Digital wallets

Investments (stocks, mutual funds, crypto, etc.)

Cash on hand

Add them all up.

Step 2: List everything you owe (Liabilities)

Include:

Credit card balances

Loans

Money you owe people

Any other debts

Add these up too.

Step 3: Subtract

Assets minus liabilities. That number is your current net worth.

Why should you care?

How These Three Numbers Actually Fit Together

Each of these numbers answers a different question about your money. On their own, they’re incomplete. Together, they tell you where you really stand.

Your income statement tells you how much money you had to work with this year.

Your spending review tells you what it costs to live your current life. This number explains why saving felt easy or impossible, regardless of how much you earned.

Your net worth snapshot is the outcome. It shows what accumulated after a year of earning, spending, saving, and borrowing.

When you look at the three together, the picture becomes clear.

If income went up but net worth didn’t, your spending increased.

If income stayed the same but net worth grew, your saving more/spending decreased.

If net worth went down, spending or debt outpaced income.

Final Thoughts

Money works the same way every time: Income minus spending, adjusted for debt, shows up as net worth. That’s your financial standing.

Next week, we’ll take everything you’ve seen here and turn it into direction. We’ll set financial goals for 2026 that fit your numbers, your goals, and your life as it really is.