- The Ipon Challenge

- Posts

- 🏦 UITFs: The Investment Your Bank Has Been Trying to Sell You (And Should You Buy?)

🏦 UITFs: The Investment Your Bank Has Been Trying to Sell You (And Should You Buy?)

UITFs explained for Filipino investors: what they are, how they work, types, fees, historical yields, and how to start investing with as little as ₱1,000.

Marianne Lim

April 06, 2026

We’ve talked about mutual funds, ETFs, and index funds in previous issues. Now let’s talk about their close cousin – the UITFs.

In today’s edition, we’ll go over:

What a UITF is

Types of UITFs

How it is different from Mutual Funds and Index Funds

Pros and Cons

How to Start

TLDR;

The Bottom Line

UITFs pool your money with other investors and let a fund manager invest it for you (in stocks, bonds, or both). They live inside your bank app, require as little as ₱1,000 to start, and are a solid first step into investing. The tradeoff is fees and no PDIC coverage. If you want something simple and accessible, it's hard to argue against starting here.

The content

What Is a UITF?

Source: Manulife Facebook Page

UITF stands for Unit Investment Trust Fund. Fancy name, simple idea.

You pool your money with other investors. A professional fund manager takes that pool and invests it in stocks, bonds, government securities, or some mix of all three, depending on what type of fund you picked. In return, you own units of that fund. The value of your units goes up (or down) based on how the underlying investments perform.

Think of it like a group order. Instead of buying one share of Ayala Corp on your own, you and hundreds of other investors chip in together, and a fund manager buys a whole basket of securities on everyone's behalf. Your slice of that basket is your units.

The price of each unit is called the NAVpu (Net Asset Value per unit). If you invested when NAVpu was ₱1.50 and it's now ₱1.80, you've made 20%.

The Types of UITFs

Banks in the Philippines usually offer four types:

Money Market Funds invest mostly in short-term government securities and time deposits. Lowest risk, lowest return. Think of it as a slightly better savings account. You're not going to get rich, but you won't lose sleep either. Historical average returns: roughly 3–5% per year.

Bond Funds go into medium to long-term fixed-income instruments like government bonds (T-bills, T-bonds) and sometimes corporate bonds. A bit more volatile than money market, but historically yields around 4–7% annually.

Balanced Funds split exposure between equities and fixed income. You get some upside from stocks without going full equity. Returns have historically landed between 5–10% annually, but it swings more.

Equity Funds are almost entirely invested in stocks, usually tracking the PSE or a selection of blue chips. Highest risk, highest potential return. Over a 10-year horizon, Philippine equity UITFs have returned anywhere from 6–12% annually, but there were years it dropped 20–30% too. 2020 was brutal.

Real Examples You've Probably Walked Past

BDO Equity Fund — actively managed, heavier concentration on large-cap Philippine stocks. Minimum: ₱5,000.

BPI Short Term Fund — a money market UITF, good for parking cash short-term with slightly better returns than a savings account. Minimum: ₱1,000.

A quick note: we practice what we preach.

The Ipon Challenge is currently invested in a UITF, specifically BPI's Philippine Stock Index Fund. If you’ve been following us a for a while, you know what I’m talking about.

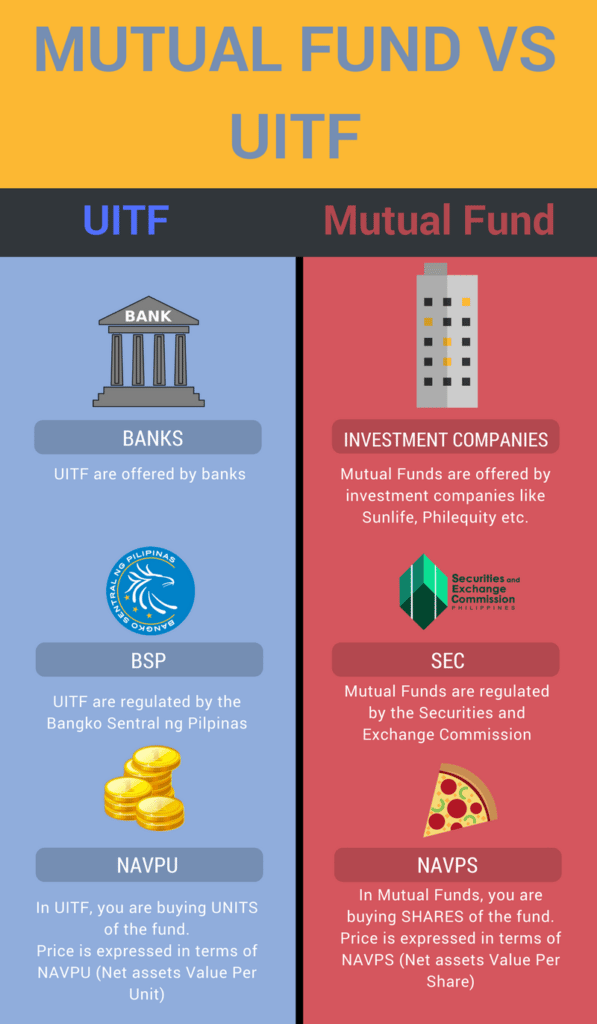

Wait, How Is This Different From Mutual Funds, Index Funds, and ETFs?

From the outside, they all look like the same thing, but the differences are actually pretty meaningful.

Source: Steemit

Mutual funds are almost identical to UITFs in structure, the only real difference is who regulates them. UITFs fall under the BSP, mutual funds under the SEC, sold by companies like Sunlife and Philam.

Index funds aren't a separate product — it's just a strategy. Some UITFs are index funds. ETFs trade on the stock exchange like stocks, are cheaper to hold long-term, but need a brokerage account to access.

The short version: same family, different wrappers. UITFs are the most accessible entry point if you already have a bank account and zero desire to open anything else.

Actionable Tips for You

The Pros and Cons

Why people like UITFs:

Low minimum entry (as low as ₱1,000)

Professionally managed, so you don't need to pick stocks yourself

Diversified by default

Liquid, though redemption settlement takes a few days

Regulated by the BSP

What people don't tell you:

Fees eat into your returns. UITFs charge a management fee (usually 1–2% per year) and sometimes a trust fee. That's deducted from NAVpu daily, quietly, whether the fund performs or not.

No PDIC coverage. Unlike your savings account, UITFs are not insured. If the fund loses money, that's on you.

Early redemption fees. Some funds charge you if you pull out within 30–90 days.

You don't control what's inside. You're trusting the fund manager's decisions entirely.

How to Start

Open a bank account if you don't have one already. BPI, BDO, and Metrobank all have solid UITF offerings.

Log into your bank app and look for "Invest" or "UITF" in the menu.

Pick your fund type based on your time horizon. Parking money for 1–2 years? Money market. Investing for 5+ years and can stomach volatility? Equity. Most of the time, there’s an extra step wherein you have to complete a risk assessment form.

Start with whatever you can afford. Seriously, ₱1,000 is enough to begin.

Check your NAVpu periodically, but don't obsess. UITFs are not day-trading instruments.

Final Thoughts

The UITF won't make you rich overnight. But it's a legitimate first step into investing, better than letting your money sit idle, and approachable enough that you'll actually start.

And starting, always, beats waiting for the perfect moment.