- The Ipon Challenge

- Posts

- 💸 The Cost of Not Letting Go. Money Mental Models #3: The Sunk Cost Fallacy

💸 The Cost of Not Letting Go. Money Mental Models #3: The Sunk Cost Fallacy

Learn how the sunk cost fallacy affects your spending and investing decisions, and how to avoid wasting more money on past choices.

Marianne Lim

March 17, 2026

Have you ever been halfway through a bad movie, already thinking it’s not worth your time, but you keep watching anyway because you’ve already started?

You sit through the next hour hoping it gets better. It usually doesn’t.

That urge to continue something just because you’ve already put time into it shows up in money and in life more often than we realize.

This week, let’s continue our recurring segment in this newsletter called Mental Models for Money.

These aren’t tactics or rules. They’re ways of thinking that help you focus on what matters, without needing to be an expert or constantly disciplined.

Last time, we talked about the power of compounding. This week, we’re talking about the sunk cost fallacy — and how it affects the way you spend, invest, and make decisions.

In today’s edition, we’ll go over:

What is Sunk Cost Fallacy

What This Means for Your Personal Finances

How This Applies to Investing (and to Life)

What this Mental Model is used for

TLDR;

The Bottom Line

The sunk cost fallacy keeps you stuck in decisions because of past spending. Focus on what makes sense today, not what you’ve already lost.

The content

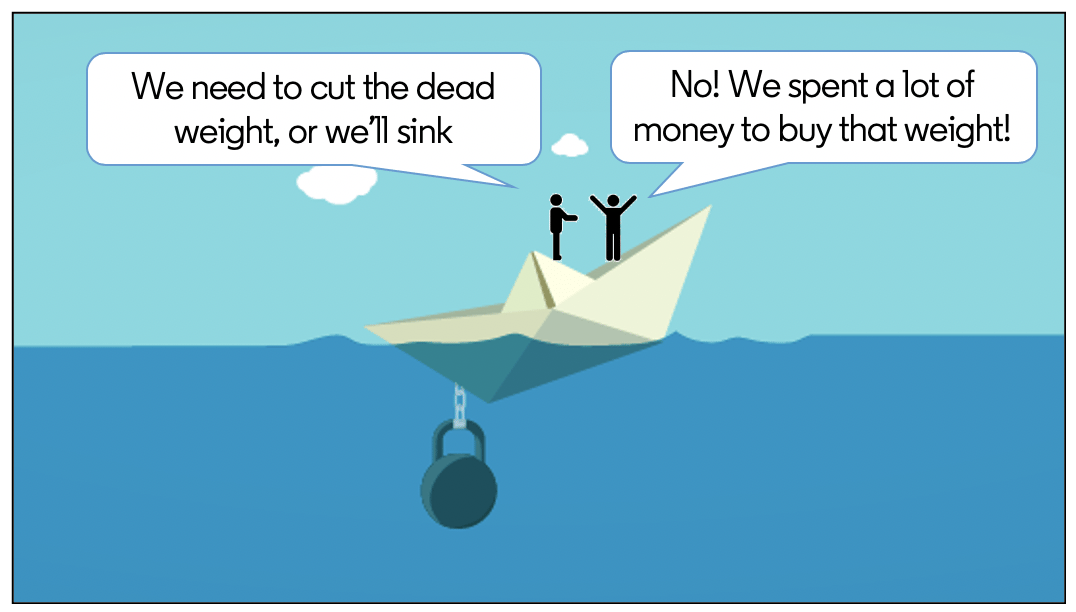

The Sunk Cost Fallacy Explained

Source: LinkedIn

The sunk cost fallacy shows up when past spending starts influencing present decisions.

You’ve already spent the money, or the time, or the effort. Walking away feels like a loss, so you continue.

But sunk costs are unrecoverable. Whether you continue or stop, the money doesn’t come back. The time doesn’t return. The only thing you control is what you do next.

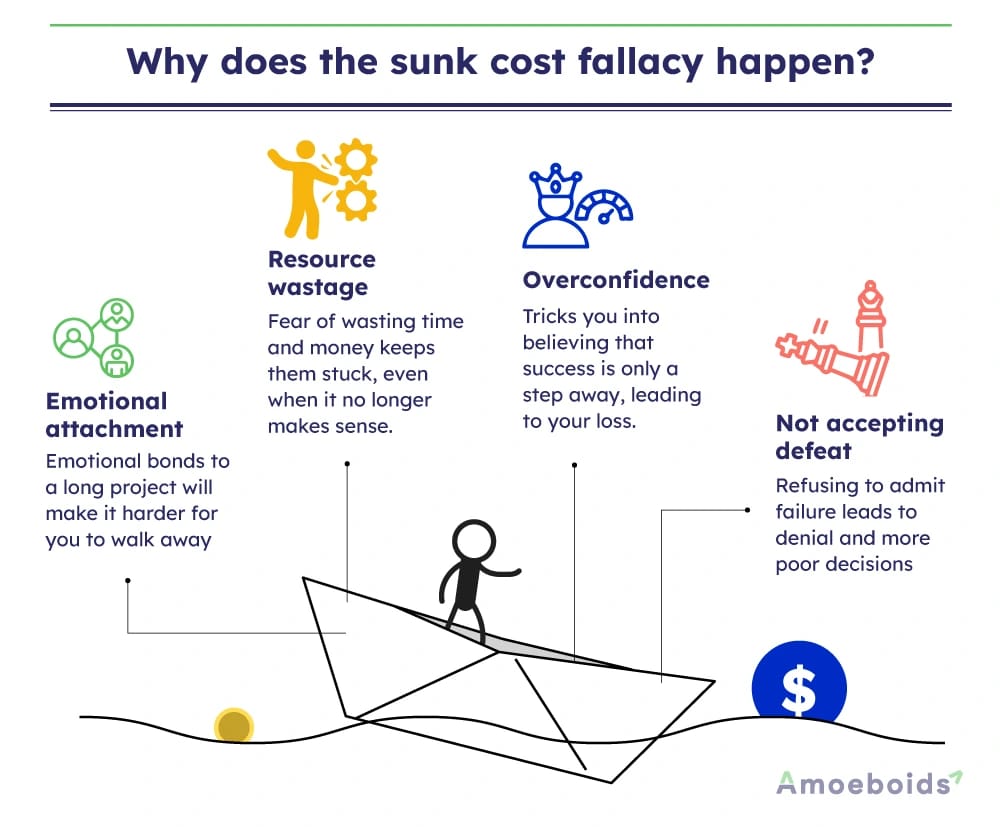

What This Means for Your Personal Finances

This shows up in everyday spending.

Source: Amoeboids

You keep a subscription you barely use because you already paid for it. You continue a gym membership you stopped enjoying. You hold on to something expensive that no longer fits your life because selling it feels like accepting a loss.

In each case, the decision shifts from evaluating value to justifying past spending.

In practice, this might mean:

cancelling mid-cycle

selling at a lower price

stopping something unfinished

None of these feel comfortable. But they prevent further loss.

The cost has already happened. Continuing just extends it. Instead of losing once, you lose repeatedly.

Why should you care?

How This Applies to Investing (and to Life)

In investing, this shows up when people hold losing positions too long. They wait for prices to return to their entry point. The market reflects current conditions. Your purchase price is personal.

The same pattern appears outside investing. You stay in a job you hate because you’ve been working there for 10 years and you’re scared to start from scratch. Projects, roles, or relationships continue simply because you’ve already invested in them.

Over time, this creates drag.

What This Mental Model Is Useful For

This model helps when something feels hard to let go of.

It applies when:

you keep something out of habit

you want to “get your money’s worth”

you delay decisions that feel like losses or “sayang naman”

It brings the focus back to current value.

A Way to Reflect on This

Think about one thing you’re holding onto. This could be a job, a relationship, or an investment

Now remove the history.

If you didn’t already have it, would you choose it today? If the answer is no, then the decision is straightforward.

The cost is already paid. The only question left is whether you want to keep paying.